Replacement Cost

In simple terms, this provision gives you coverage for your home or property to be rebuilt or replaced like new, without depreciation for age, wear and tear, etc. Nearly every homeowners policy that we see has some kind of replacement cost coverage. Not all replacement cost provisions are the same. There are 2 basic options:

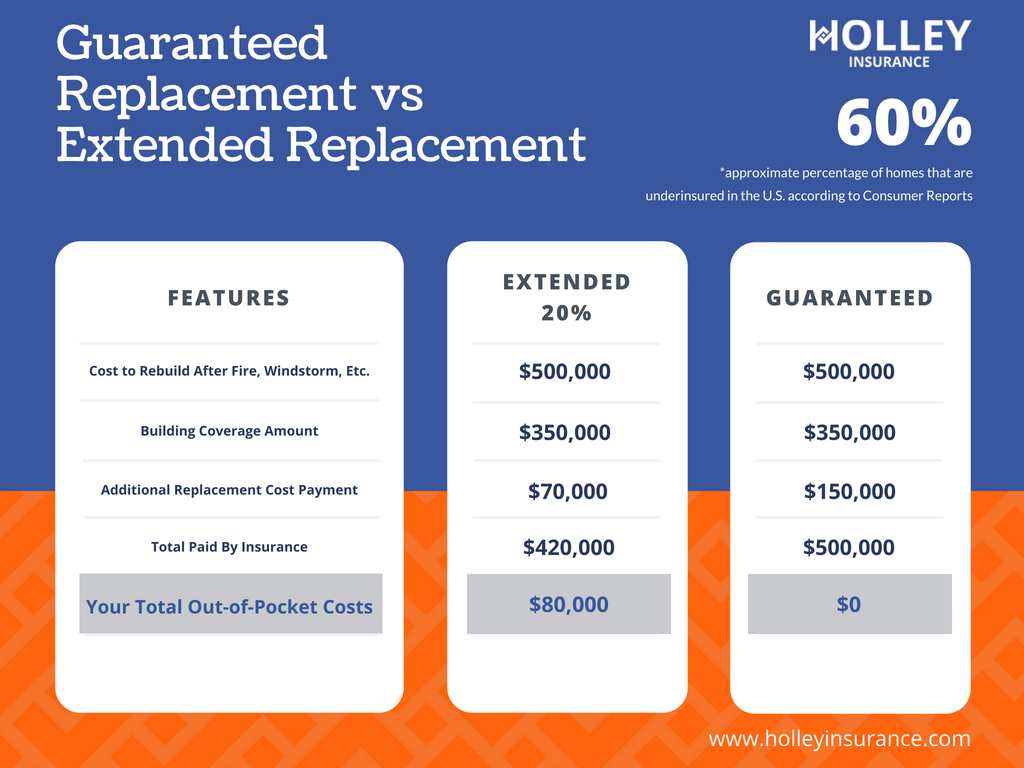

- Extended or Limited Replacement - This provides for extra coverage (anywhere from 20-50%) above the Dwelling coverage. As an example, a home insured at $250,000 with 20% Extended Replacement cost coverage could get up to an additional $50,000 in coverage should the $250,000 not be adequate to replace the home.

- Guaranteed Replacement - This is exactly what it sounds like and what most people mistaken believe that they have. This provision says that the insurance company is required to pay for the actual replacement cost of a home at the time of the loss, even if it extends well above the actual amount of coverage shown for the dwelling. So, in our example above, the home insured at $250,000 dwelling coverage could be covered for $300,000, $500,000, or what ever amount is required to replace it with like kind and quality. This is far superior to Extended or Limited Replacement.

Some agents will downplay the importance of having Guaranteed Replacement. After all, they have performed replacement cost estimate and get a pretty good idea of what it costs to rebuild. Don’t fall for this trap.

Consumer Reports found that about 60% of homes are underinsured by an average of 20%. That means that at the time of a claim, they may not be able to actually replace their homes despite having “replacement cost” coverage.

The problem gets even worse in areas that are hit by large natural disasters like wild fires or tornados. When a tragic event like that happens, demand for building supplies, contractors, etc. goes way up, as do their prices.

All of a sudden, a home that could normally be built for $200 per square foot may cost more than twice that. This leaves the homeowner holding the bag for the difference, unless they buy a guaranteed replacement cost policy.

Here is a sample claims illustration to show the difference between an underinsured home with Guaranteed vs Extended 20% Replacement Cost coverage.